The United States and Israel have launched coordinated military operations against Iran, targeting key elements of the regime’s military and strategic infrastructure and triggering a wider regional response across the Gulf.

Putting aside questions about the legitimacy of U.S. action, how should investors, particularly Christian investors, think about what is unfolding in the Middle East?

This moment should not be viewed simply as another regional conflict or a limited confrontation with Iran. What is taking shape reflects something broader. The escalation in the Middle East is occurring at a time when the economic and geopolitical framework that shaped much of the modern global economy is beginning to shift.

For many years, global markets operated under the assumption that economic interdependence would reduce conflict and stabilize international relations. Supply chains stretched across continents, energy flowed across oceans, and capital moved freely across borders in pursuit of higher returns. Efficiency became the defining principle of globalization, reinforcing the belief that deeper economic integration would gradually align the interests of nations.

That assumption is now under strain.

The central question, therefore, is not whether one agrees with the tactics being used in the current conflict. Rather, the question investors must consider is what these developments signal about the direction of the global economic system and how capital should be stewarded in a world where geopolitical alignment increasingly matters alongside economic efficiency.

The current escalation in the Middle East intersects with a broader geopolitical pattern unfolding across multiple regions of the world. What is happening in the Gulf connects to strategic pressure points stretching from Latin America to the North Atlantic and the Arctic. These developments should not be viewed as isolated crises but rather as interconnected pieces of a larger strategic puzzle.

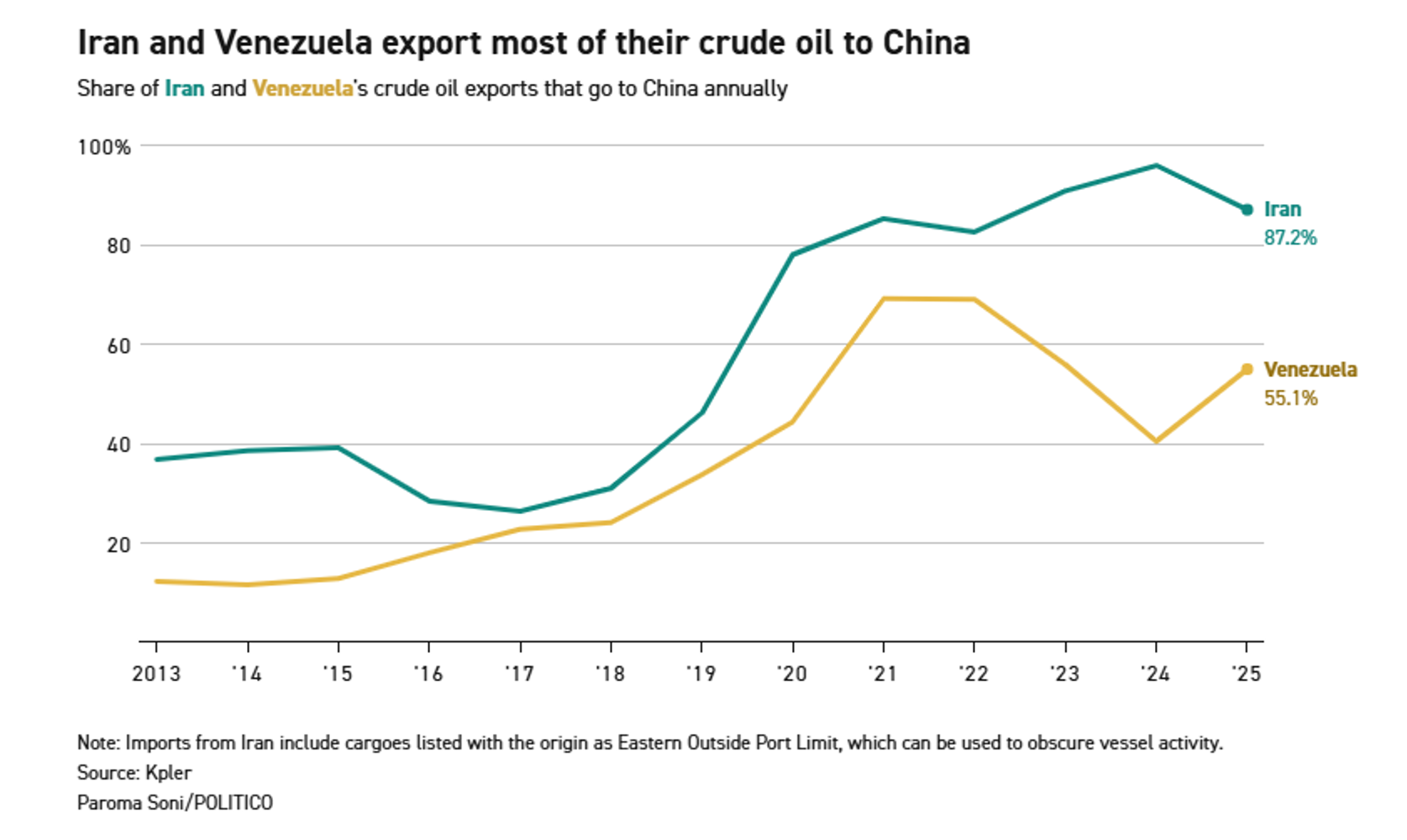

Iran sits at the center of one axis of this competition, particularly through its energy relationship with China. In recent years China has been by far the largest buyer of Iranian crude, absorbing more than 80 percent of Iran’s exported oil in certain periods.

At the same time, developments in Venezuela illustrate how Latin America has again become an arena of great power competition. Venezuela’s oil exports have become heavily dependent on China, with well over half of Venezuelan crude shipments flowing to Chinese buyers. Russia has backed Maduro’s Venezuela diplomatically and economically while simultaneously deepening cooperation with Iran.

Pressure on Venezuela has already reshaped the political and energy landscape across the Caribbean basin, where countries such as Cuba depend heavily on Venezuelan support. If current trends continue, the strategic focus of competition may increasingly shift toward the Caribbean as well, where the legacy alliances of the Cold War intersect with the great power competition of the twenty-first century.

Strategic geography is also returning to the center of global politics. Control of trade corridors such as the Panama Canal has again become a geopolitical priority, while locations that once seemed peripheral to markets, such as Iceland in the North Atlantic, are gaining renewed importance because of their role in Arctic shipping routes and the strategic corridor linking North America and Europe.

Across Europe, policymakers increasingly speak about sovereignty, defense capacity, and energy independence. The belief that trade alone guarantees stability has weakened, replaced by a growing recognition that security alignment now matters as much as economic integration.

Globalization as the organizing principle of the world economy is fading, while geopolitical alliances are becoming more central to how nations structure trade, energy flows, and capital movement.

The Abraham Accords initially emerged as a diplomatic breakthrough that normalized relations between Israel and several Sunni Arab states. At the time, they were widely viewed as incremental progress within a complex and fragile region.

Recent events suggest those agreements may represent something far more consequential.

Iran’s retaliation across Gulf states has accelerated years of gradual realignment that had already been underway beneath the surface. In attempting to project strength across the region, Tehran may have unintentionally clarified the strategic interests of its neighbors. Moments of crisis often reveal alliances that had previously remained tentative or informal.

The United States and Israel have led the initial wave of strikes targeting Iranian military and strategic infrastructure. Yet they are not operating in isolation. Several Sunni Arab states that historically maintained distance from Israel are now playing roles in the broader response.

Saudi Arabia has opened airspace and logistical channels supporting coalition operations. Qatar has taken defensive action after Iranian missile strikes targeted its territory and U.S. installations hosted there. The United Arab Emirates, Bahrain, and other Gulf states have also been drawn into the conflict after facing drone and missile attacks launched by Iranian forces.

The conflict has also begun to brush against the broader NATO security architecture. Turkey, a NATO member positioned at the crossroads of Europe and the Middle East, has already been pulled into the regional security dynamics as Iranian missiles and military activity have crossed airspace and threatened the eastern Mediterranean corridor. As tensions escalate, NATO’s defensive posture in the region may increasingly come into play, further widening the strategic implications of the conflict.

These alignments would have been difficult to imagine a decade ago. Countries that once stood on opposite sides of regional diplomacy are now operating within the same security architecture. American military power, Israeli technological and intelligence capabilities, and Gulf state geography and financial strength are increasingly converging into a coordinated strategic posture.

Wars tend to drag when coalitions fracture. They compress when alignment becomes decisive.

The emerging alignment between the United States, Israel, and several Sunni Arab states increases the likelihood that this conflict may prove shorter rather than longer. When regional actors share intelligence, airspace, logistics, and strategic objectives, military pressure concentrates more quickly and the timeline of conflict can compress.

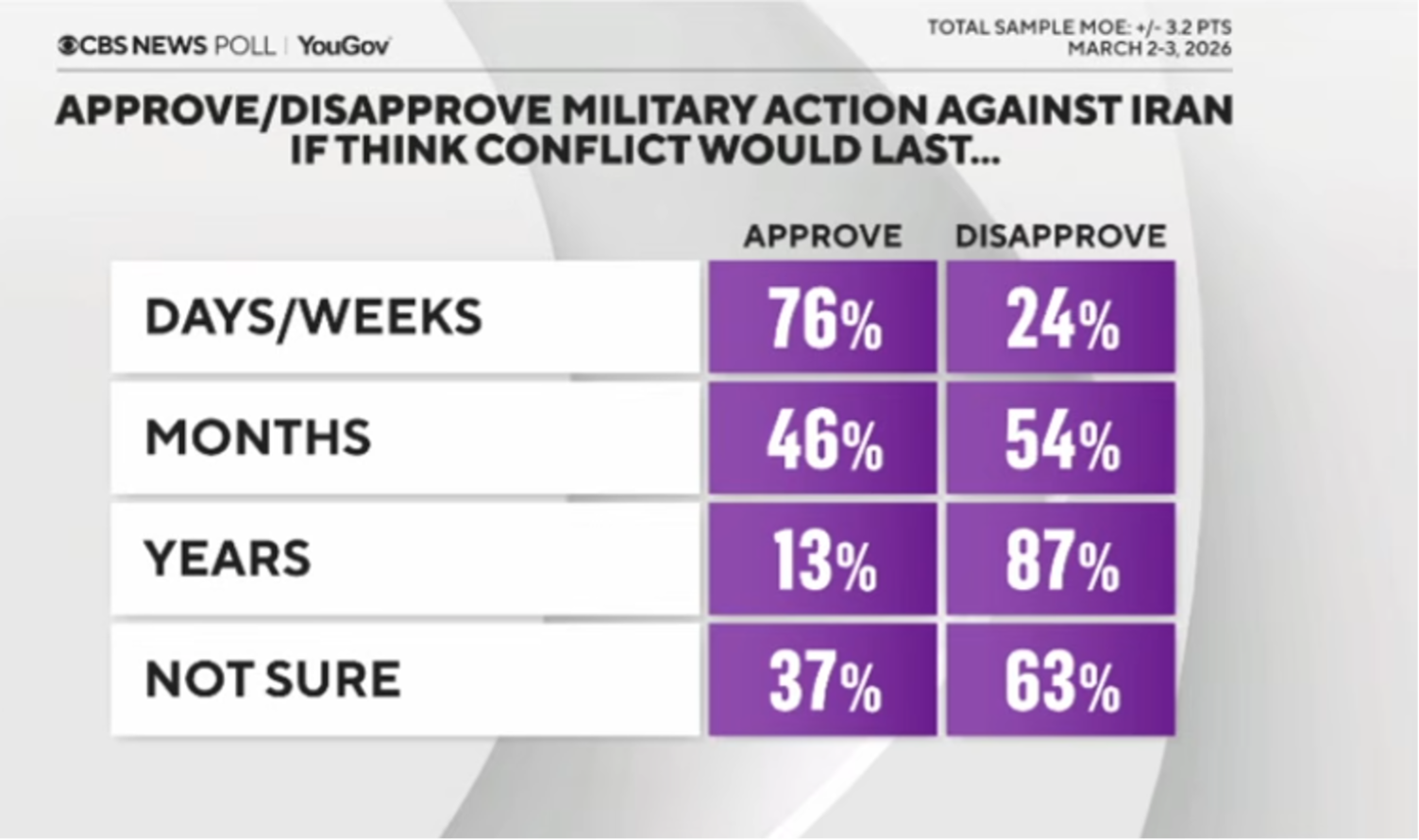

This dynamic matters not only militarily but politically. American public support for military action is often closely tied to expectations about duration. Recent polling illustrates this clearly. Support for military action against Iran rises sharply when Americans believe the conflict will last only days or weeks, while support declines significantly if the war is expected to stretch into months or years.

In other words, the public appears willing to support decisive action but remains deeply wary of another prolonged conflict in the Middle East.

If the coalition now forming across the region remains aligned, the strategic objective may be a rapid shift in regional balance rather than a prolonged military occupation. That distinction will matter greatly for markets and for political confidence at home.

For investors, this shift does not imply economic collapse, but it does suggest the emergence of a different operating environment. Globalization helped create powerful disinflationary forces as expanding global labor pools and highly optimized supply chains suppressed costs across industries for many years. A world that places greater emphasis on resilience, domestic production, and defense capability is likely to operate with somewhat higher structural inflation floors over time.

.png)

Markets also enter this period from a position of elevated valuations. When inflation floors rise and geopolitical risk premiums return, valuation multiples can compress even in the absence of recession. An overvalued market does not require economic collapse to correct. It requires uncertainty.

Given the geopolitical realignment now unfolding before our eyes, investors should prepare for a different operating environment in the years ahead:

It is also worth remembering that markets do not always behave rationally in the short term. Historically, stock market declines tied to geopolitical events have often been relatively modest and short-lived, frequently averaging around five percent before recovering.

For Christian investors, moments like this require both moral clarity and investment discipline. Geopolitical conflicts affect real people and real nations, reminding us that stewardship involves responsibilities beyond financial markets.

The world economy is entering a new phase where geopolitics, alliances, and national security will play a larger role in shaping markets than they have for much of the past generation. Short-term volatility does not change long-term investment principles. Emotional reactions to headlines can undermine years of careful planning, which is why thoughtful counsel matters. If you have questions about how these developments affect your portfolio, consult your advisor and keep decisions anchored to long-term objectives.

Tim Schwarzenberger, CFA is a Portfolio Manager and Director of Corporate Engagement for Inspire Investing. He previously served as Managing Director at Christian Brothers Investment Services (CBIS), where he was an integral member of the Investment Team responsible for implementing the firm’s strategy development, portfolio construction, and Catholic investing initiatives.

The United States and Israel have launched coordinated military operations against Iran, targeting key elements of the regime’s military and strategic infrastructure and triggering a wider regional response across the Gulf.

Putting aside questions about the legitimacy of U.S. action, how should investors, particularly Christian investors, think about what is unfolding in the Middle East?

This moment should not be viewed simply as another regional conflict or a limited confrontation with Iran. What is taking shape reflects something broader. The escalation in the Middle East is occurring at a time when the economic and geopolitical framework that shaped much of the modern global economy is beginning to shift.

For many years, global markets operated under the assumption that economic interdependence would reduce conflict and stabilize international relations. Supply chains stretched across continents, energy flowed across oceans, and capital moved freely across borders in pursuit of higher returns. Efficiency became the defining principle of globalization, reinforcing the belief that deeper economic integration would gradually align the interests of nations.

That assumption is now under strain.

The central question, therefore, is not whether one agrees with the tactics being used in the current conflict. Rather, the question investors must consider is what these developments signal about the direction of the global economic system and how capital should be stewarded in a world where geopolitical alignment increasingly matters alongside economic efficiency.

The current escalation in the Middle East intersects with a broader geopolitical pattern unfolding across multiple regions of the world. What is happening in the Gulf connects to strategic pressure points stretching from Latin America to the North Atlantic and the Arctic. These developments should not be viewed as isolated crises but rather as interconnected pieces of a larger strategic puzzle.

Iran sits at the center of one axis of this competition, particularly through its energy relationship with China. In recent years China has been by far the largest buyer of Iranian crude, absorbing more than 80 percent of Iran’s exported oil in certain periods.

At the same time, developments in Venezuela illustrate how Latin America has again become an arena of great power competition. Venezuela’s oil exports have become heavily dependent on China, with well over half of Venezuelan crude shipments flowing to Chinese buyers. Russia has backed Maduro’s Venezuela diplomatically and economically while simultaneously deepening cooperation with Iran.

Pressure on Venezuela has already reshaped the political and energy landscape across the Caribbean basin, where countries such as Cuba depend heavily on Venezuelan support. If current trends continue, the strategic focus of competition may increasingly shift toward the Caribbean as well, where the legacy alliances of the Cold War intersect with the great power competition of the twenty-first century.

Strategic geography is also returning to the center of global politics. Control of trade corridors such as the Panama Canal has again become a geopolitical priority, while locations that once seemed peripheral to markets, such as Iceland in the North Atlantic, are gaining renewed importance because of their role in Arctic shipping routes and the strategic corridor linking North America and Europe.

Across Europe, policymakers increasingly speak about sovereignty, defense capacity, and energy independence. The belief that trade alone guarantees stability has weakened, replaced by a growing recognition that security alignment now matters as much as economic integration.

Globalization as the organizing principle of the world economy is fading, while geopolitical alliances are becoming more central to how nations structure trade, energy flows, and capital movement.

The Abraham Accords initially emerged as a diplomatic breakthrough that normalized relations between Israel and several Sunni Arab states. At the time, they were widely viewed as incremental progress within a complex and fragile region.

Recent events suggest those agreements may represent something far more consequential.

Iran’s retaliation across Gulf states has accelerated years of gradual realignment that had already been underway beneath the surface. In attempting to project strength across the region, Tehran may have unintentionally clarified the strategic interests of its neighbors. Moments of crisis often reveal alliances that had previously remained tentative or informal.

The United States and Israel have led the initial wave of strikes targeting Iranian military and strategic infrastructure. Yet they are not operating in isolation. Several Sunni Arab states that historically maintained distance from Israel are now playing roles in the broader response.

Saudi Arabia has opened airspace and logistical channels supporting coalition operations. Qatar has taken defensive action after Iranian missile strikes targeted its territory and U.S. installations hosted there. The United Arab Emirates, Bahrain, and other Gulf states have also been drawn into the conflict after facing drone and missile attacks launched by Iranian forces.

The conflict has also begun to brush against the broader NATO security architecture. Turkey, a NATO member positioned at the crossroads of Europe and the Middle East, has already been pulled into the regional security dynamics as Iranian missiles and military activity have crossed airspace and threatened the eastern Mediterranean corridor. As tensions escalate, NATO’s defensive posture in the region may increasingly come into play, further widening the strategic implications of the conflict.

These alignments would have been difficult to imagine a decade ago. Countries that once stood on opposite sides of regional diplomacy are now operating within the same security architecture. American military power, Israeli technological and intelligence capabilities, and Gulf state geography and financial strength are increasingly converging into a coordinated strategic posture.

Wars tend to drag when coalitions fracture. They compress when alignment becomes decisive.

The emerging alignment between the United States, Israel, and several Sunni Arab states increases the likelihood that this conflict may prove shorter rather than longer. When regional actors share intelligence, airspace, logistics, and strategic objectives, military pressure concentrates more quickly and the timeline of conflict can compress.

This dynamic matters not only militarily but politically. American public support for military action is often closely tied to expectations about duration. Recent polling illustrates this clearly. Support for military action against Iran rises sharply when Americans believe the conflict will last only days or weeks, while support declines significantly if the war is expected to stretch into months or years.

In other words, the public appears willing to support decisive action but remains deeply wary of another prolonged conflict in the Middle East.

If the coalition now forming across the region remains aligned, the strategic objective may be a rapid shift in regional balance rather than a prolonged military occupation. That distinction will matter greatly for markets and for political confidence at home.

For investors, this shift does not imply economic collapse, but it does suggest the emergence of a different operating environment. Globalization helped create powerful disinflationary forces as expanding global labor pools and highly optimized supply chains suppressed costs across industries for many years. A world that places greater emphasis on resilience, domestic production, and defense capability is likely to operate with somewhat higher structural inflation floors over time.

Markets also enter this period from a position of elevated valuations. When inflation floors rise and geopolitical risk premiums return, valuation multiples can compress even in the absence of recession. An overvalued market does not require economic collapse to correct. It requires uncertainty.

Given the geopolitical realignment now unfolding before our eyes, investors should prepare for a different operating environment in the years ahead:

It is also worth remembering that markets do not always behave rationally in the short term. Historically, stock market declines tied to geopolitical events have often been relatively modest and short-lived, frequently averaging around five percent before recovering.

For Christian investors, moments like this require both moral clarity and investment discipline. Geopolitical conflicts affect real people and real nations, reminding us that stewardship involves responsibilities beyond financial markets.

The world economy is entering a new phase where geopolitics, alliances, and national security will play a larger role in shaping markets than they have for much of the past generation. Short-term volatility does not change long-term investment principles. Emotional reactions to headlines can undermine years of careful planning, which is why thoughtful counsel matters. If you have questions about how these developments affect your portfolio, consult your advisor and keep decisions anchored to long-term objectives.

.png)

.png)